Preparing Your Small Business for a Commercial Loan: What Lenders Look for and How to Get Ready

Getting ready to apply for a commercial loan? Learn what lenders look for and how small businesses can prepare for approval with confidence.

Getting ready to apply for a commercial loan? Learn what lenders look for and how small businesses can prepare for approval with confidence.

Buying an existing daycare or early education center involves more than financials. Learn what buyers should evaluate before purchasing to avoid hidden costs and operational challenges.

Considering an SBA loan? This guide explains what business owners need to know before applying, from requirements to common mistakes and financing strategies.

Thinking about buying a restaurant? From evaluating financials and lease terms to assessing location, equipment, and operations, this guide breaks down what you need to know before you invest—so you can move forward with confidence and clarity.

Buying an existing gas station can be one of the most efficient and profitable ways to enter the fuel and convenience retail industry. Compared to building a station from the ground up, purchasing an established operation offers immediate cash flow, lower startup risk, and access to proven locations with existing customer demand.

For entrepreneurs, investors, and first‑time owners alike, understanding the advantages of buying an existing gas station can help drive smarter acquisition decisions and long‑term success.

One of the biggest advantages of buying an existing gas station is immediate income. Unlike new construction projects—where revenue may be months or years away—an operational station is already generating sales from fuel, convenience store merchandise, and often additional services like food, car washes, or lottery.

With an established operation, buyers can:

This financial visibility makes it easier to plan budgets, secure financing, and begin earning returns immediately after closing.

In the gas station business, location is everything. When you buy an existing gas station, you’re investing in a site that has already proven its value.

An operating station confirms:

Instead of guessing whether a new corner or roadway will attract drivers, buyers can evaluate real‑world performance data—significantly reducing risk.

Most existing gas stations benefit from repeat customers who stop by out of habit, convenience, and trust. This built‑in customer base provides a reliable foundation for ongoing sales and future growth.

Benefits include:

Even under new ownership or a new brand, the location itself often retains customer familiarity and value.

Buying an existing gas station means acquiring a business with core systems already functioning. These typically include:

Rather than building everything from scratch, owners can focus on improving efficiency, reducing shrinkage, and increasing profitability—an especially valuable advantage for first‑time buyers.

Financing is often more accessible when purchasing an established gas station. Lenders prefer investments with a documented financial track record, and an existing operation provides exactly that.

Buyers benefit from:

If you’re looking to buy an existing gas station and need help with gas station financing or identifying proven locations, working with experienced professionals is critical. Commercial Resources specializes in helping buyers navigate financing options while identifying profitable gas station opportunities that align with their investment goals.

Developing a new gas station involves zoning approvals, environmental reviews, tank installations, permitting, and construction—each carrying potential delays and cost overruns.

An existing gas station already has:

While thorough due diligence is still essential, buying an existing location significantly reduces the uncertainty associated with new development.

Modern gas stations generate income far beyond fuel sales. Depending on the location, an existing station may already include:

This allows buyers to immediately assess which revenue streams are performing well—and where improvements can drive rapid growth.

Many gas stations are under‑optimized due to absentee ownership or outdated operating practices. New owners can unlock value by:

These improvements can quickly increase revenue and significantly raise the long‑term value of the property.

Buying an existing gas station is a major investment, and having the right expertise can help buyers avoid costly mistakes. If you’re searching for gas station locations for sale, need help with financing, or want guidance through the acquisition process, Commercial Resources provides specialized commercial real estate insight focused on gas station and convenience store transactions.

Their experience helps buyers make informed decisions with confidence.

Buying an existing gas station offers immediate cash flow, proven locations, established operations, and meaningful growth potential. For entrepreneurs and investors looking to enter the fuel and convenience industry efficiently, an established station provides a strong foundation with reduced risk and faster returns.

With solid due diligence and experienced guidance, purchasing an existing gas station can be both a profitable business and a long‑term investment opportunity.

Many business owners secured SBA 7(a) loans at a time when interest rates were historically low. Today, those same loans—often structured with adjustable rates—are becoming increasingly expensive as rates fluctuate upward. For companies that value predictable cash flow and long‑term stability, this creates an important question:

Is there a better financing structure for the long haul?

For owner‑occupied commercial real estate, the answer is often yes—and it comes in the form of an SBA 504 refinance.

SBA 7(a) loans are flexible and widely used, but many are tied to the Prime Rate and adjust periodically. As interest rates rise, borrowers can experience:

For businesses that rely on steady financial planning, these variables can introduce unnecessary risk.

The SBA 504 refinance program is designed specifically for long‑term assets like owner‑occupied commercial real estate. Its defining feature is long‑term, fixed‑rate financing, which contrasts sharply with the variable nature of most 7(a) loans.

A typical 504 refinance structure includes:

This structure allows businesses to replace uncertainty with stability.

SBA 504 debentures offer fixed rates for 20 or 25 years, helping business owners insulate themselves from future rate increases. This predictability supports more confident long‑term planning.

By refinancing into a longer, fixed amortization, many businesses can reduce monthly debt service, freeing up cash for working capital, staffing, or reinvestment.

Because the SBA 504 program typically requires no additional cash beyond standard equity levels, borrowers can preserve liquidity rather than tying up funds in refinancing costs.

For businesses that occupy at least 51% of their building, the SBA 504 refinance aligns financing terms with the reality of owning and operating commercial property—long‑term, stable, and growth‑oriented.

An SBA 504 refinance may be a strong fit if:

Even if your existing loan is relatively new, it may still be worth evaluating your options in today’s rate environment.

At Commercial Resources, we view financing as more than a transaction—it’s a tool that should support your business strategy. Refinancing a variable‑rate SBA 7(a) loan into a fixed‑rate SBA 504 structure can help reduce risk, enhance predictability, and strengthen your financial foundation over time.

For business owners navigating today’s interest‑rate landscape, the right refinancing decision can make a meaningful difference for years to come.

Managing cash flow is one of the most essential skills for any small business owner. Even profitable businesses can struggle — or fail — if cash isn’t flowing in at the right time. Understanding how money moves in and out of your business gives you the power to plan, grow, and stay resilient during slow seasons or unexpected expenses.

Cash flow is the movement of money into (inflows) and out of (outflows) your business.

Even if revenue looks strong on paper, delayed payments, rising expenses, or seasonal demand can leave your bank account depleted.

You can be profitable without being cash‑flow positive.

For example:

You might land a big contract, but if the customer doesn’t pay for 60 days and you need to cover payroll tomorrow, you have a cash flow problem — not a profitability problem.

Cash flow directly affects your ability to:

Profit is long‑term.

Cash flow is day‑to‑day survival.

Understanding where your cash comes from helps identify strengths and risks.

Everyday business activities: sales, services, vendor payments, wages, taxes.

Buying or selling long‑term assets: equipment, vehicles, property.

Loans, credit lines, owner investments, or dividend payouts.

Operating cash flow is the heartbeat of your business. If it’s consistently negative, something fundamental must change.

Here are practical steps you can implement immediately:

Weekly reviews prevent surprises. Look for patterns:

Aim for at least 1–3 months of operating expenses in reserve.

This buffer protects you from late payments or seasonal dips.

Project your cash position 30, 60, and 90 days ahead.

This helps you anticipate shortages before they hit.

✔ Track real deposits — not promised payments.

✔ Create a tax savings account and set aside a percentage of every sale.

✔ Keep inventory levels aligned with real demand.

✔ Audit subscriptions, service fees, and supply costs quarterly.

✔ Use separate accounts so cash flow is easy to track and analyze.

The tool matters less than consistency.

Mastering cash flow isn’t just good financial practice — it’s a competitive advantage. Businesses that understand and monitor cash flow run more smoothly, make better decisions, and stay strong even during unpredictable times.

Whether you’re brand new or growing fast, cash flow is the foundation. When you manage it well, everything else becomes easier.

Buying a business that includes commercial real estate can be one of the most profitable long‑term investment decisions you make. Not only do you acquire a revenue‑generating company, but you also secure the land and building that support the business—often increasing stability, value, and future cash‑flow potential. To make a smart purchase, buyers must learn how to evaluate commercial real estate when buying a business with confidence and accuracy.

Below are the essential factors every buyer should examine during the due‑diligence process.

Before you finalize any purchase, evaluate the physical condition of the property. A commercial inspection should include:

Deferred maintenance or upcoming major repairs can significantly affect the deal—and may be used to negotiate a lower purchase price.

Zoning restrictions can support or block business operations. Confirm:

If the business model depends on expansion, outdoor operations, or extended hours, zoning compatibility is non‑negotiable.

Commercial real estate value is heavily influenced by location. Consider:

A strong location boosts both business performance and property appreciation.

When the property includes tenants—or has space that could be leased out—buyers should evaluate the real estate as an income‑producing asset. Key metrics include:

This is especially important for retail plazas, warehouses, or mixed‑use buildings.

Environmental problems can create major liability. Depending on the business type, you may need:

Issues uncovered here should be addressed before closing.

Commercial real estate can be valued using several approaches:

A professional appraisal is essential when financing through SBA or conventional lenders.

Buying a business with real estate opens additional financing opportunities:

Real estate often improves loan approval odds because lenders view it as stronger collateral.

Knowing how to evaluate commercial real estate when buying a business ensures that you protect your investment, negotiate intelligently, and maximize your return. With proper due diligence, buyers can acquire not just a business—but a long‑term real estate asset that continues to appreciate and generate wealth.

Expanding or purchasing a daycare center can be an exciting next step for early childhood professionals looking to grow their impact — but it often requires significant financial investment. Whether you’re opening a second location, renovating an existing space, or acquiring an established center, the right financing strategy can make the process smoother, smarter, and more affordable.

This guide breaks down the most effective funding options for daycare owners and the steps you can take to secure the financing you need.

Before seeking financing, create a clear picture of how much capital you’ll need. Common costs include:

A detailed budget not only guides your financial decisions but also strengthens your funding applications.

Daycare businesses are uniquely eligible for a variety of funding sources because they support essential community childcare needs. Below are popular financing pathways.

SBA loans are one of the most common financing tools for daycare owners thanks to competitive interest rates and long repayment terms.

Best SBA programs for child care centers:

These loans require a strong business plan, good credit, and financial documentation, but they offer some of the most favorable terms available to small business owners.

If your daycare has a proven track record of success and stable revenue, banks may offer competitive business loans. These are ideal for:

Banks may require collateral, tax returns, cash flow statements, and business projections.

Depending on your state, there may be grants available for early learning providers. These can support:

While grants can be competitive and time‑limited, they’re worth pursuing because they do not require repayment.

If your goal is to purchase a building for your center, a commercial real estate loan may be the right option. These loans typically offer:

These can be combined with SBA backing for even more favorable terms.

If you already own a center, a business line of credit can be a flexible way to fund:

You only pay interest on what you use, making it a good tool for short‑term or phased projects.

If you’re buying an existing daycare, sometimes the seller will partially finance the sale. This:

Negotiating these terms can make the purchase far more accessible.

Lenders and investors want to see that you understand the daycare business and have a realistic path to profitability.

Your plan should include:

A well‑built business plan increases approval odds dramatically.

Before applying for financing, take these steps:

The more financially stable you appear, the better your financing terms will be.

Financing for daycare centers can be complex. Bringing in an expert can help you:

This is especially helpful for new owners or multi‑site expansions.

Think beyond the loan approval. Sustainable daycare growth requires:

Good financial management ensures you stay attractive to lenders later — and keep your center thriving.

Securing financing to buy or expand a daycare is absolutely achievable with preparation, clarity, and the right funding strategy. Whether you pursue SBA loans, grants, bank financing, or seller support, your investment will help bring high‑quality childcare to more families — a win for both your business and your community.

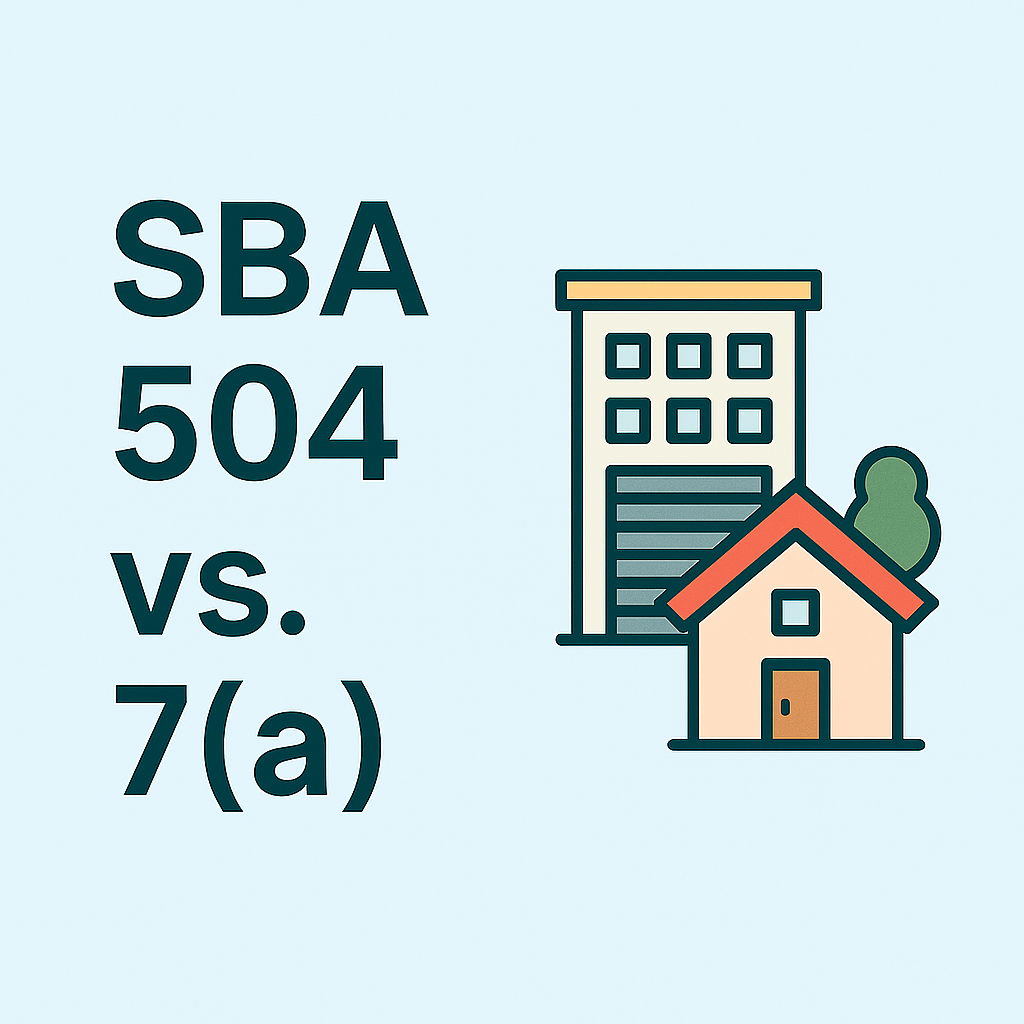

When a small business is ready to purchase a building, expand into a larger space, or finance major renovations, two SBA loan programs dominate the conversation: SBA 504 and SBA 7(a). Both can be used for commercial real estate, but they differ significantly in structure, terms, and best‑use scenarios.

This guide breaks down the key differences so business owners can choose the best option.

An SBA 504 loan is designed specifically for fixed‑asset purchases, including owner‑occupied commercial real estate. These loans are known for:

According to SBA program guidelines, businesses can use SBA 504 loans for real estate, construction, or building improvements, making them ideal for companies looking to buy property they will occupy.

A typical 504 loan includes:

The SBA 7(a) program is the SBA’s most flexible financing option, covering a wide range of uses beyond real estate—working capital, refinancing, equipment, and more.

SBA 7(a) loans can be used for commercial real estate when the business will occupy at least 51% of the property. They also offer:

NerdWallet confirms that both 7(a) and 504 programs can be used for commercial real estate, but 7(a) loans offer greater flexibility for borrowers who may need working capital alongside the purchase.

| Feature | SBA 504 Loan | SBA 7(a) Loan |

|---|---|---|

| Best Use | Buying or improving commercial real estate | Real estate + broader business uses |

| Rates | Typically lower, fixed | Fixed or variable |

| Down Payment | 10–20% | Typically ~10% |

| Max Loan Size | Up to ~$5.5M (CDC portion) | Up to $5M |

| Speed | Moderate | Slower, more paperwork |

| Flexibility | Limited—real estate only | High—can include working capital |

| Occupancy Rule | 51% minimum | 51% minimum |

If your main goal is buying or expanding into a building, the SBA 504 loan is usually the superior option due to its interest rates, structure, and terms.

But if you need flexibility, or if your project includes cash‑flow needs alongside real estate, the SBA 7(a) loan may be the better fit.