If your business is carrying high-interest debt tied to real estate or equipment, an SBA 504 refinance could be one of the smartest financial moves you make.

With today’s evolving interest rate environment, now is the perfect time to check your rate and explore how refinancing can improve your cash flow, stability, and long-term growth.

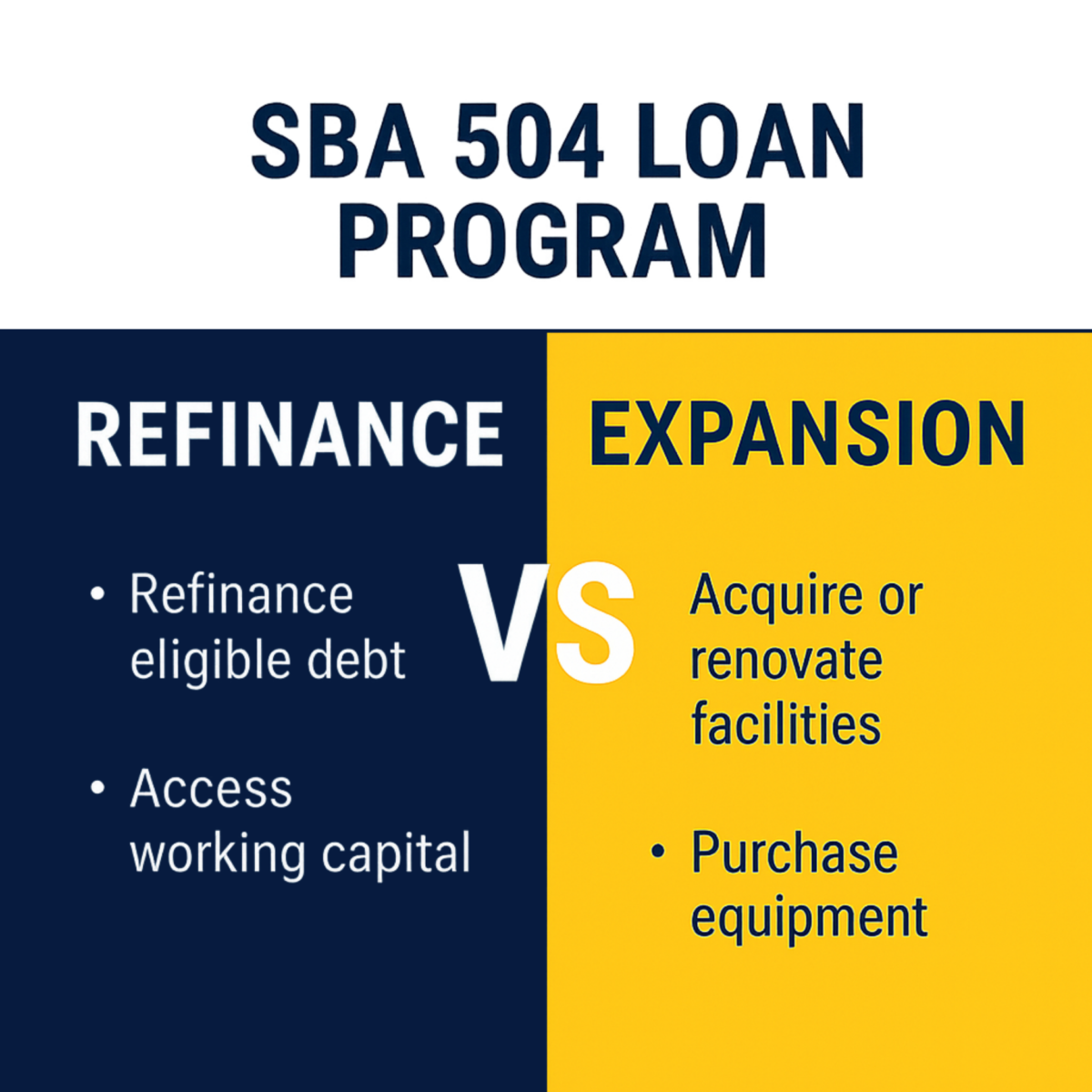

What Is an SBA 504 Refinance?

The SBA 504 Loan Program was designed to help small businesses secure long-term, fixed-rate financing for major assets like commercial real estate and equipment.

Through refinancing, the SBA 504 program allows you to:

- Replace existing commercial debt

- Lock in lower, fixed interest rates

- Access equity for business needs

This is a powerful option for businesses currently dealing with variable rates or higher-cost traditional loans.

Key Benefits of an SBA 504 Refinance

✅ 1. Lower Monthly Payments

Refinancing into a longer-term, fixed-rate structure often reduces your monthly payment, freeing up capital for operations, hiring, or expansion.

✅ 2. Fixed Interest Rates = Predictability

Unlike fluctuating rates, SBA 504 loans offer stable, long-term fixed rates, helping you plan your finances with confidence.

✅ 3. Improved Cash Flow

Lower payments plus stable rates = healthier cash flow, which is critical for:

- Covering operating expenses

- Investing in growth opportunities

- Weathering economic uncertainty

✅ 4. Access to Equity

If your property has appreciated, refinancing may allow you to pull out usable equity to reinvest into your business.

✅ 5. Consolidate Business Debt

You may be able to combine multiple loans into one, simplifying your finances and reducing overall interest costs.

✅ 6. Strengthen Your Balance Sheet

Refinancing into better terms can improve your financial profile—making your business more attractive to lenders and investors.

Who Qualifies?

An SBA 504 refinance is ideal for businesses that:

- Own and occupy commercial real estate

- Have existing debt tied to that property

- Are looking to lower rates or improve cash flow

- Have been operating for at least 2 years (in most cases)

Even if you’re unsure, it’s worth taking a closer look—many businesses qualify sooner than they expect.

Why Now Is the Time to Check Your Rate

Interest rates shift constantly, and many businesses are still carrying loans secured during less favorable conditions.

That means you could be:

- Paying more than necessary

- Missing out on long-term savings

- Limiting your growth potential

A simple rate check could reveal significant savings opportunities.

Real Impact: What Refinancing Can Do

Businesses that refinance using SBA 504 loans often see:

- Lower operating stress

- More available working capital

- Better long-term planning ability

- Increased profitability over time

It’s not just about saving money—it’s about positioning your business for success.

Take the Next Step: Check Your Rate

Refinancing doesn’t have to be complicated. The first step is simple:

👉 Check your current rate and explore your options

By comparing your existing loan with SBA 504 refinancing, you can quickly determine if there’s an opportunity to:

- Save money

- Improve cash flow

- Strengthen your business

Final Thoughts

An SBA 504 refinance is more than a financial adjustment—it’s a strategic move that can give your business the stability and flexibility it needs to grow.

If you haven’t reviewed your loan recently, now is the time.

✅ Lower your rate

✅ Improve your cash flow

✅ Invest back into your business

🚀 Ready to see what you qualify for?

Check your rate today and take control of your financial future.